Key Points

- NSW cattle supply has been tracking well ahead of 5 and 10-year averages for most of “liquidation” – I foresee more heavy supply in 2025 as well.

- Weaner steers, bought by feedlots have ticked over A$10/kg lwt in the US saleyard system.

- A tale of two halves this week with all southern Australian markets coming under price pressure whilst the northern markets found some short term confidence amid shorter supplies – boosted by timely falls of rain, particularly for QLD.

Supply

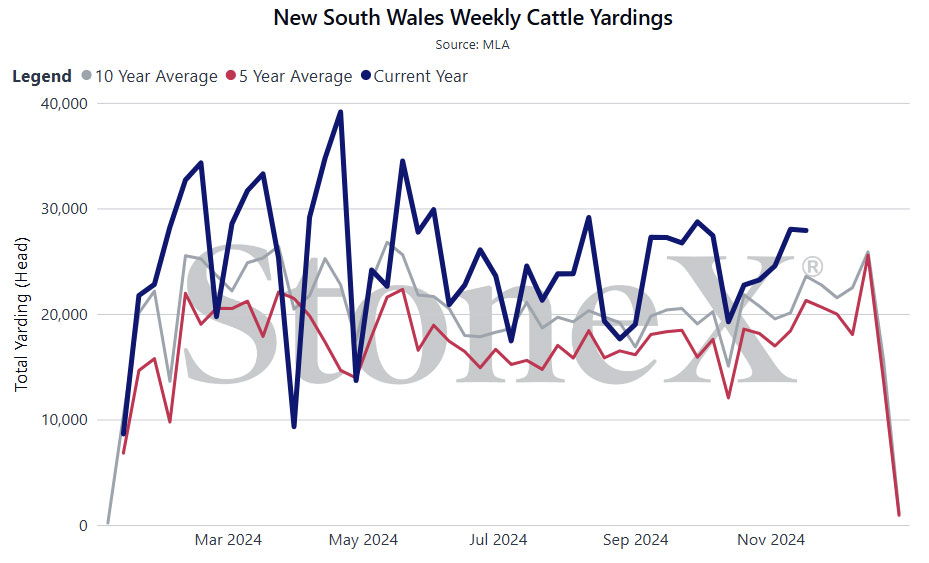

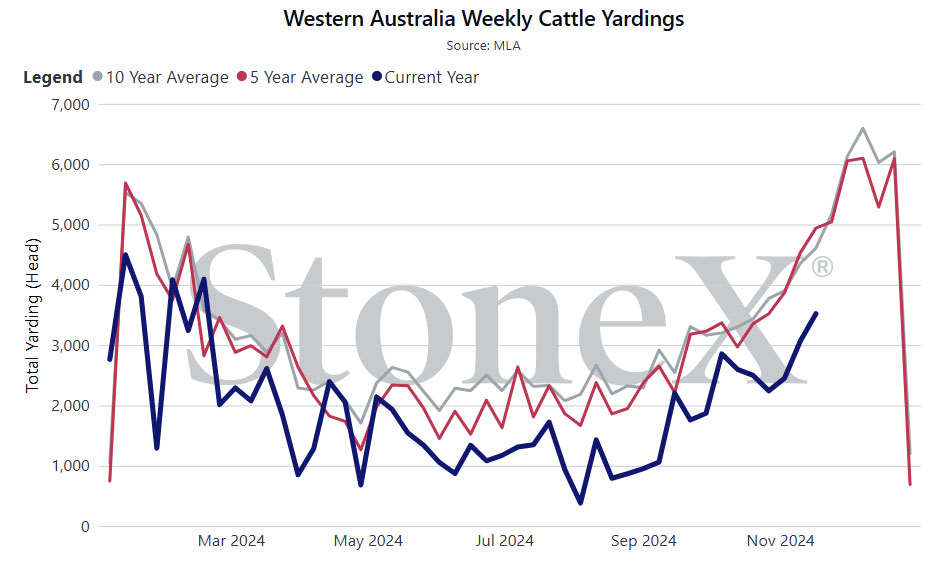

- As per the above (which is available via StoneX Market Information platform) NSW cattle supply well ahead of 5 and 10-year weekly averages and has been operating that way for most of 2024, whilst WA cattle supply continues to lag well behind longer term averages and has done for just about every week in 2024.

- The heightened NSW supply seen over 2024 speaks directly to the size of the cattle herd in NSW, more numbers on farm translate to more marketings. Higher saleyard numbers despite a move towards direct sales for many producers reaffirms the herd size point.

- Weaker supply out of WA is an interesting one, seemingly this points towards producers choosing direct sales channels marketing of livestock but it although may mean we see strong lifts in saleyard supply in early 2025 for the state out of the yards.

- Movements of cattle have slowed in QLD over the past week which is contributing to some upward pressure on grids and saleyard markets, although conversely, a number of areas, particularly NSW, which received rain have seen supply increase regardless, this translated into an overall lift in numbers week-on-week in the yards.

- This has happened a number of times over spring and indicates that producers are recognising the need to sell rather than retain, with weights (for most places) already exceeding expectations due to season and pushing towards the top end of grids which brings discounts into play.

Demand

- Tighter supply this week has certainly forced the hand of some feedlots which may be operating hand to mouth on small orders to lift their rates to secure stock.

- Restocker demand did improve in places, although the hot weather due in the next week could stifle any further improvement in that demand as feed bases dry off.

Price

- A draft of 182 weaner steers, destined for the feedlot at the Oklahoma National Stockyards in the US on Tuesday weighing 216kg/head on average (478lb) made A$11/kg or A$2,391/head.

- Back on home soil, it’s definitely been a tale of two halves across the eastern seaboard, southern NSW, SA & VIC prices softened, the falls they’ve had over the past week have done little to improve pasture bases as feed goes rank and the season cuts out.

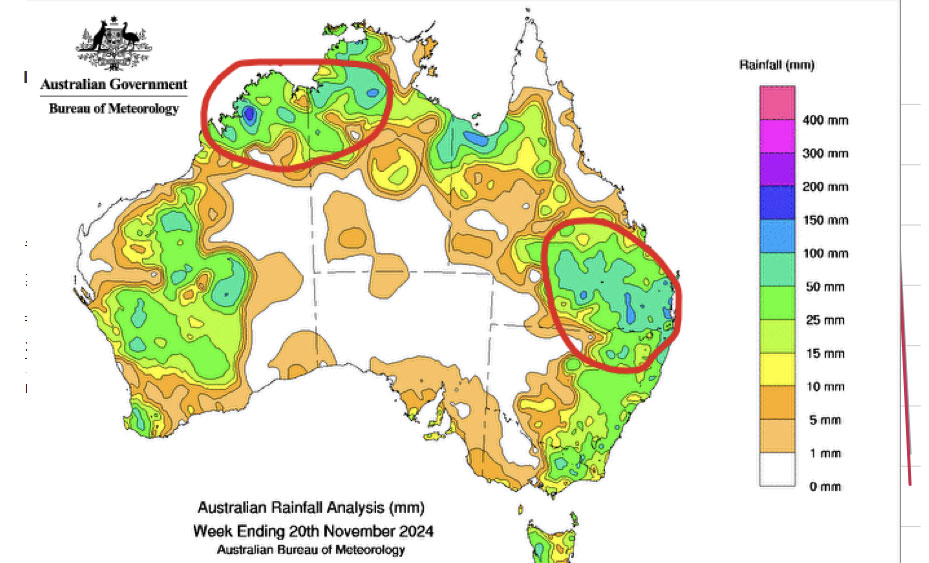

- Rain in parts of northern NSW, central and southern QLD (over a week 150mm + in parts) has seen that market liftà this rain was needed and timely for a lot of producers, particularly in QLD, with the drier weather over the past few months posing challenges.

- Heavy cattle continue to come under pressure, the softening US imported CL market is flowing back through to Australian prices, at a point when domestic US beef cow slaughter numbers rise à although this year cow slaughter (seasonally) is well down on previous years due to the US simply running out of cows.

Weather

- The rainfall across central and southern QLD into northern NSW over the past week has generally been widespread, albeit stormy.

- Its these falls that have reinstalled some confidence into the QLD market whereby despite steady to higher supply (producers selling on the premise of rising prices) the market did improve, particularly for the big saleyard centres of Roma & Dalby.

- Early storms across the north west of the country in the Kimberley & VRD regions à the wet is expected to start later with storms beginning in December to see the monsoonal season kick off, further falls for most of the territory and north east WA on the way over the next week as well.

- I’ll be watching how the wet season tracks for the north, another average to above average season will see further herd growth in the north to offset southern herd declines, higher fertility rates and improved mortalities will be the drivers.

- As per the above (which is available via StoneX Market Information platform) NSW cattle supply well ahead of 5 and 10-year weekly averages and has been operating that way for most of 2024, whilst WA cattle supply continues to lag well behind longer term averages and has done for just about every week in 2024.

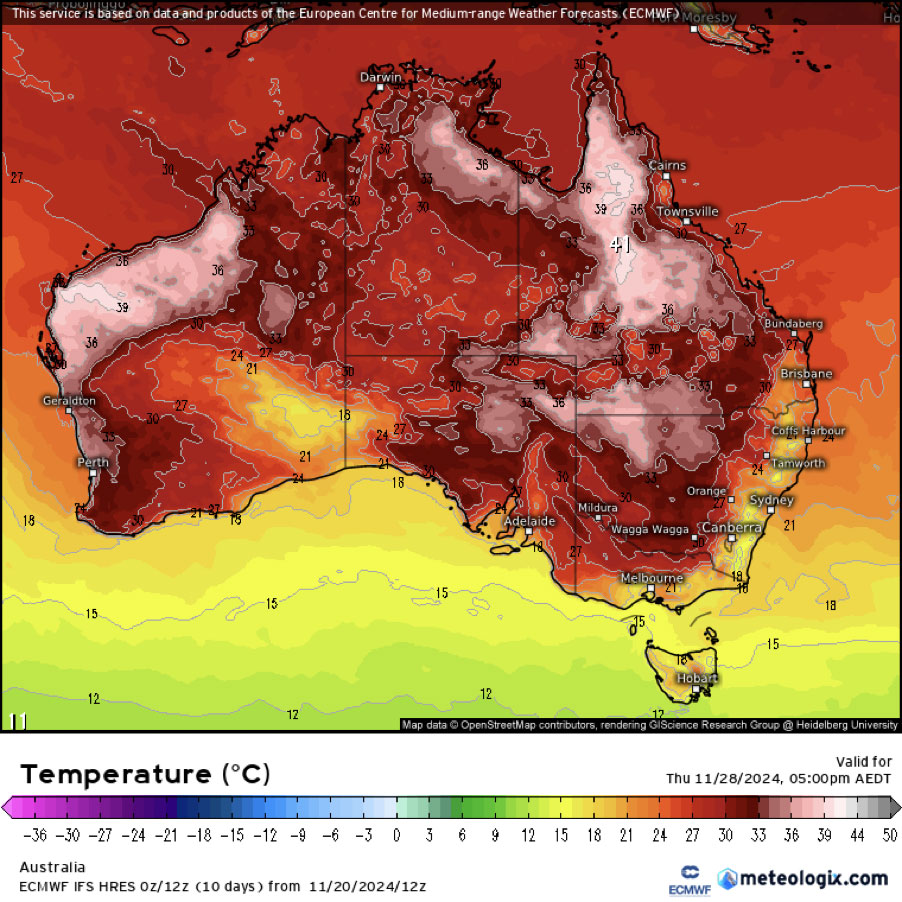

- ECMWF 7 day temperature outlook above, with a sharp rise in temperatures again following rain, this may quickly effect the rain that has fallen, particularly north of Dubbo into QLD.

- Heat will then translate to impacts on cattle performance in feedlots and on grass and grazing behaviour, something to be cognisant of.

Ripley Atkinson | Australian Livestock & Commodities Manager

M: +61 427 417 803

www.stonex.com | ripley.atkinson@stonex.com

StoneX Financial Pty Ltd (ACN 141 774 727 | ABN 50 141 774 727)

Suite 28.01 | 264 George Street | Sydney | NSW | Australia

NASDAQ: SNEX

StoneX Disclaimer

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI. StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.